Financial Education

Your path to financial health

GreenPath Financial Wellness

Your financial health is our priority, so we’ve partnered with GreenPath Financial Wellness to offer you financial counseling, guidance, and educational resources. Many services are free of charge, and GreenPath can also assist with specialized programs that may include a fee. GreenPath is here to support you in making decisions that make your life easier.

Experts you can trust

GreenPath has more than 60 years of experience helping people build financial health and resiliency. Their NFCC and HUD-certified counselors explain your options to manage credit card debt and mortgage debt, learn about personal finance, and come up with a plan to make your financial goals happen. Below are a few of the most popular programs from Greenpath.

Financial Counseling

You have access to one-on-one financial counseling delivered by caring, certified experts. Understand your situation, learn about options, and make a plan to reach your goals.

Home Buying Counseling

If you have housing goals or concerns, GreenPath’s HUD-certified housing counselors can help. Take advantage of foreclosure prevention services, homebuyer counseling, rental counseling, and reverse mortgage counseling.

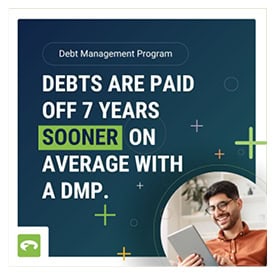

Debt Management Program

If you have high-interest credit card debt, a GreenPath Debt Management Plan may be able to help lower your interest rates so you can pay off debt faster while saving money.

Webinars and more

Take advantage of monthly educational webinars, articles, and online learning designed to strengthen your financial health.

Disclosures

-

Seattle Credit Union partners with GreenPath Financial Wellness to provide financial counseling and education services to our members. GreenPath is an independent third‑party provider. When you use GreenPath services, any information you choose to share is provided directly to GreenPath and is governed by their privacy practices, terms, and conditions.